The Printed Circuit Board (PCB) is the fundamental interconnect carrier for all electronic products, often termed the “central nervous system of the electronics industry.” From smartphones and automotive electronics to communication equipment, industrial controls, aerospace, and medical devices, virtually every system containing electronic components relies on PCBs.

The explosive growth of emerging applications such as 5G, AI, IoT, new energy vehicles, and humanoid robots continuously elevates requirements for PCB layer count, precision, materials, and integration, driving an upgrade across the entire industry chain. This article will systematically present the PCB industry ecosystem and explore future opportunities and challenges through four sections: Industry Chain Structure → Key Segments & Company Profiles → Case Studies & Data → Trends & Outlook.

1、PCB Industry Chain Structure

The PCB production process can be simplified into three major segments: Upstream → Midstream → Downstream, each containing multiple sub-sectors and representative companies.

Upstream: Raw Materials & Equipment

- Copper Clad Laminate (CCL): The foundational substrate of PCBs, composed of resin, glass fiber cloth, and copper foil. Key materials include:

- Copper Foil: Electrolytic copper foil and rolled copper foil.

- Glass Fiber Fabric (E-glass, NE-glass): A key reinforcement material for CCL.

- Resin: Epoxy resin, polyimide (PI), BT resin, etc..

- Chemical Solutions: Etchants, plating solutions, developers, etc..

- Production Equipment: Drilling machines, exposure equipment, plating lines, laminating presses, Automated Optical Inspection (AOI) equipment, etc..

Midstream: PCB Manufacturing

- Design & Engineering Services: PCB layout, Design for Manufacturability (DFM) analysis.

- Manufacturing Process: Cutting → inner layer imaging → lamination → drilling → plating (desmear/electroless copper/electroplating) → outer layer imaging → surface finish (HASL, ENIG, OSP, immersion silver, etc.) → routing → testing → final inspection.

- Classification by Layer Count: Single-sided, double-sided, multilayer boards (common 4-16 layers, servers/communication can reach 20-40+ layers), High-Density Interconnect (HDI), rigid-flex boards, IC substrates.

Downstream: Application End-Markets & EMS Assembly

- Application Fields: Consumer electronics (phones, tablets, laptops), communication equipment (base stations, switches, routers), automotive electronics (ADAS, BMS, autonomous driving domain controllers), industrial control, medical electronics, aerospace, defense, etc..

- EMS/ODM Manufacturers: Companies that assemble PCBs and components into modules or final products (e.g., Foxconn, Pegatron, Quanta).

2、Key Segments & Company Profiles

Upstream Raw Materials

- CCL Manufacturers: This segment forms the cost base of PCBs, accounting for approximately 27-40% of total cost.

- Shengyi Technology (China): A global leader in CCL production, covering standard FR-4 to high-frequency, high-speed CCL for 5G base stations and servers. It is a key supplier to Huawei and ZTE.

- Nanya New Materials (China): A core domestic supplier of high-frequency, high-speed CCL, rapidly advancing in technology.

- Taiwanese & Japanese Leaders: Companies like ITEQ, Elite Material Co. (EMC), and Panasonic dominate the high-end speciality CCL market (e.g., M7, M8, M9 grades for AI servers), which is crucial for AI hardware. Rogers Corporation (US) holds a technological high ground in high-frequency microwave materials (PTFE-based) for radar and satellite communication.

- Copper Foil Manufacturers: Electrolytic copper foil is a major CCL raw material, constituting about 30-50% of its cost.

- Defu Technology & Tongguan Copper Foil (China): Considered leaders in electronic copper foil in China, with products entering the NVIDIA AI server supply chain. High-end varieties like HVLP (Hyper Very Low Profile) foil are critical for high-speed signals.

- Norden (Nuode) & Jiayuan Technology (China): Companies with dual focus on lithium battery foil and electronic circuit foil.

- Mitsui Mining & Smelting (Japan): A leading supplier of high-end rolled copper foil for fine-line HDI and rigid-flex boards.

- Specialty Glass Fabric/Resin: Key for performance enhancement.

- Glass Fabric: Philippe (China) is the global leader in quartz fiber fabric (Q-cloth), having secured exclusive capacity from NVIDIA. Honghe Technology (China) leads in ultra-thin electronic fabric. China Jushi has the largest sales volume of electronic fabric.

- Specialty Resins: Dongcai Technology (China) has the largest PCH (hydrocarbon resin) capacity among A-share companies. Shengquan Group supplies high-end epoxy resins.

- Equipment & Consumables Manufacturers: Direct beneficiaries of capacity expansion and technology upgrades.

- Drilling/Exposure: Han’s Laser (China) is a global leader in PCB drilling equipment. Xinji Microelectronics (China) is the domestic leader in Direct Imaging (LDI) equipment.

- Plating: Dongwei Technology specializes in plating equipment.

- Consumables: Dingtai High-Tech is a global leader in PCB drill bits.

Midstream PCB Manufacturing

Global First Tier (High-layer Count, HDI, IC Substrates):

- Zhen Ding Technology (ZDT, Taiwan): A core PCB supplier in the Apple supply chain, covering HDI, flexible printed circuits (FPC), and substrate-like PCBs.

- Unimicron (Taiwan): A powerhouse in IC substrates and high-layer count boards, serving CPU/GPU/memory chip packaging.

- Shennan Circuits (China): A domestic leader in high-layer count and communication boards, deeply involved in 5G base station and server board manufacturing. It is also a key supplier for AMD’s MI300.

- Wus Printed Circuit (China): A traditional leader in AI server and high-speed network switch PCBs, with high share among overseas core customers like NVIDIA. It is also a certified Tesla supplier for automotive boards.

- Shengyi Electronics (China): A subsidiary of Shengyi Tech, with nearly 50% of its revenue from AI server-related products, supplying major cloud clients.

Second Tier & Key Players (Mid-to-High End Multilayer, Special Application Boards):

- Kinwong (China): The global leader in automotive PCBs (supplying Tesla, BYD), also with batch orders for AI servers as a qualified NVIDIA supplier.

- Suntak Technology (China): Specializes in quick-turn and small-batch, high-mix PCB manufacturing, meeting R&D prototyping needs.

- Dongshan Precision (China): Expanded from FPC to rigid boards, serving consumer electronics and new energy sectors. It is the second-largest Apple FPC supplier.

- Avary Holdings (Zhen Ding) &DSBJ are ranked global top PCB manufacturers by revenue.

Downstream Application & EMS

- Communication Equipment OEMs: Huawei, Ericsson, Nokia (PCBs are core components for their base stations and switches).

- Automotive Tier-1 Suppliers: Bosch, Continental, Denso (requiring high-reliability PCBs for ADAS, BMS, etc.).

- EMS/ODM: Foxconn, Pegatron, Quanta, Flex (assembling PCBA into final products).

3、Case Studies & Data: Drivers of Change in the PCB Industry

Data Perspective

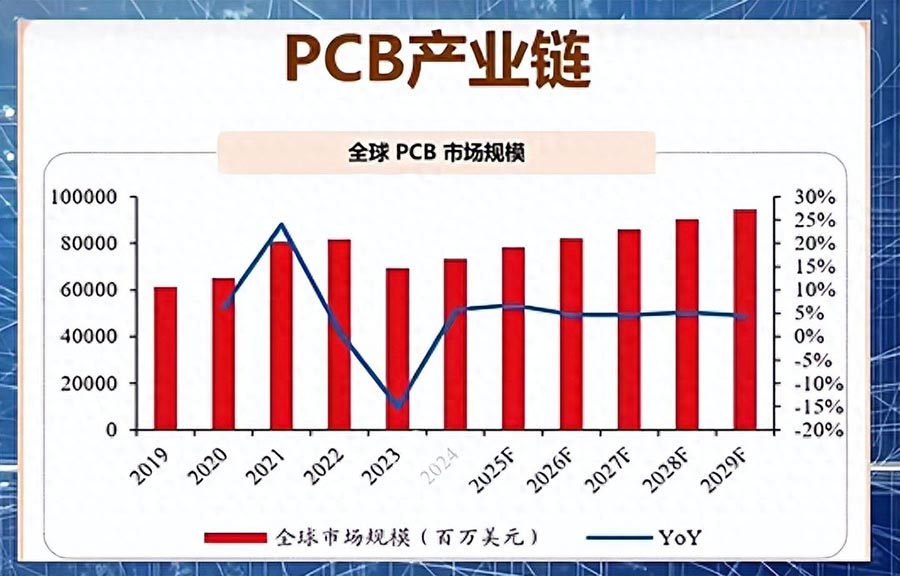

- Global Output Value: According to Prismark data, the global PCB output value was approximately 783.4billionin2023andisforecasttoreach783.4 billion in 2023 and is forecast to reach 783.4billionin2023andisforecasttoreach968 billion by 2025, driven by AI servers and automotive electronics.

- Regional Distribution: China is the core manufacturing hub, accounting for about 56% of global output value in 2024. Taiwan, Japan, and South Korea hold significant shares in high-end segments.

- Product Structure Shift: The proportion of HDI and high-layer count boards is rising annually. AI server demand is significantly driving growth for boards with 18+ layers. IC substrate demand is growing rapidly (>10% CAGR) due to AI chips and advanced packaging like Chiplet/HBM.

Typical Cases

- 5G Base Stations Drive High-Frequency Boards: The deployment of millimeter-wave base stations requires modified PTFE-based CCL and low-loss PCBs to reduce signal loss, supplied by companies like Rogers and Shengyi Tech.

- New Energy Vehicles (NEVs) Upgrade Automotive PCBs: The PCB value per intelligent electric vehicle is significantly higher than for traditional vehicles. For instance, the BMS requires PCBs resistant to high temperatures and vibration, met by suppliers like Wus through improved resin systems and copper thickness design.

- AI Servers Fuel High-Layer Count Demand: An AI training server can contain PCBs with 24-40 layers, requiring high interlayer alignment precision. This creates massive orders for companies like Shennan Circuits and Unimicron from cloud service providers. The PCB value in an NVIDIA GB200 cabinet can reach $171,000, second only to the GPU in hardware cost. Specific technologies like NVIDIA’s Rubin M9 material and orthogonal backplane (78 layers) represent the next frontier, with companies like Suntak Technology being the first to pass verification.

4、Trends & Outlook: The Leap from “Volume” to “Quality”

Technology Trends

- High-Performance Materials: Increasing demand for low-loss, high-thermal-conductivity, and extreme-environment-resistant materials, such as ceramic-filled substrates and modified polyimide (MPI) for flexible circuits.

- Finer Lines & Micro-Vias: Line width/space moving towards below 30/30 μm, micro-via diameter < 50 μm, driving upgrades in laser drilling and plating processes.

- Rigid-Flex & 3D Interconnection: Used in wearables and medical implants for space saving and multi-planar routing.

- Sustained Heat for IC Substrates: Driven by Chiplet and 2.5D/3D packaging, demand for FCBGA and SiP substrates is robust, with technical requirements approaching semiconductor packaging levels.

Market Trends

- Regional Diversification & Localization: Geopolitical factors and pandemic impacts are accelerating regional diversification of the PCB supply chain, with new capacity in Southeast Asia, while mainland China shifts towards high-end manufacturing.

- Green Manufacturing: Lead-free, low-halogen, and energy-saving processes are becoming mandatory, pushing equipment and chemical suppliers to upgrade.

- Multi-Point Application Growth: Beyond traditional communications and consumer electronics, automotive electronics, AI servers, robotics, and satellite internet are becoming new growth engines.

Challenges

- Raw Material Price Volatility: Copper prices are linked to global markets, while glass fiber and resin are significantly affected by energy costs.

- High-End Technical Barriers: IC substrates and ultra-high-layer count boards require long-term technological accumulation and substantial equipment investment, creating high entry barriers.

- Environmental & Compliance Pressure: Regulations like EU RoHS and REACH are imposing stricter limits on chemicals and processes.

5、Conclusion: Industry Chain Synergy Builds Core Competitiveness

The PCB industry does not win through isolated points but through a complete ecosystem formed by material innovation, sophisticated equipment,, and application-driven. Upstream, high-performance base materials and copper foil are the foundation of quality. Midstream, process capability and yield control determine delivery competitiveness. Downstream, evolving application demands drive the iteration of technology and materials.

Looking forward, companies must simultaneously develop capabilities in R&D, supply chain resilience, green manufacturing, and global layout to seize opportunities in high-frequency/high-speed, high-layer count, IC substrates, and other high-end fields. The current industry cycle, driven by the resonance of technological upgrade and import substitution, offers significant growth space for domestic enterprises with core technologies.